International Dry Bulk Market Weekly Comment

July 14, 2014 - July 18, 2014

Weekly Dry Bulk Observation

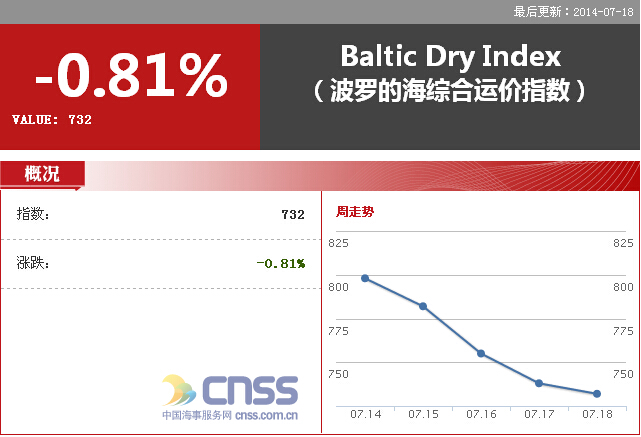

The international dry bulk market ended last week with the Baltic Dry Index (BDI) at 732 points, a decrease of 82 points (10%) from a week ago. Dry bulk rates came under pressure across the board last week, with rates for the larger vessel classes coming under significant pressure. Capesize rates are likely to rebound soon, however, as Chinese iron ore import demand remains very strong and capesize fleet growth remains low. In total, 111 dry bulk vessels were chartered in the spot market last week. This is 9 more than were chartered during the previous week. Only 6 dry bulk vessels were chartered for period deals last week, which was 5 less than the previous week.

Capesize vessels

Capesize rates ended last week averaging $8,648/day, which was a decrease of $1,604 (16%) from a week ago. Spot Australian iron ore cargo volume was strong again last week, with BHP and FMG particularly active. 17 spot Australian iron ore cargoes surfaced in the market last week, which was 3 less than the previous week but still a very firm amount. A much larger amount of Brazilian iron ore cargoes also surfaced. In total, 9 spot Brazilian iron ore cargoes surfaced last week, which was 6 more than surfaced during the previous week. The rate of the Australia-Qingdao route has risen by 1.8% to $7.650/ton. The daily cost to charter a capesize vessel for a Pacific round-trip voyage has declined by 8.8% from a week ago to $8,327/day. The rate of the Tubarao-Qingdao route has fallen by 8.5% from a week ago to $18.582/ton. The rate of the Tubarao-Rotterdam route has decreased by 12.2% from a week ago to $8.000/ton. In addition, the daily cost to charter a capesize vessel for an Atlantic round-trip voyage has decreased by 33.4% to $5,090/day. In the time charter market, the capesize time charter market was not at all active last week. No capesize vessels were chartered for period deals last week. In comparison, the previous week saw one capesize vessel chartered for a period deal.

Panamax Vessels

Panamax rates ended last week averaging $4,681/day, which was a decrease of $751 (14%) from a week ago. Panamax rates have come under renewed pressure due to ongoing vessel oversupply. The rate of the Atlantic to Far East route has declined by 7.3% from a week ago to $10,350/day. The daily cost to charter a panamax vessel for an Atlantic round-trip voyage has declined by 20.4% from a week ago to $3,888/day. The daily cost to charter a panamax vessel for a Pacific round-trip voyage has fallen by 19.4% from a week ago to $4,444/day. The rate of the Far East to Europe route has decreased by 74.6% from a week ago to $42/day. In the time charter market, the panamax time charter market was active again last week as six panamax vessels were chartered for period deals. This is two less than were chartered during the previous week. Most recently, an 80,000 dwt vessel was chartered for 3 to 6 months for $7,700/day.

Supramax Vessels

Supramax rates ended last week averaging $6,886/day, which was a decrease of $123 (2%) from a week ago. Supramax rates have been able to stay relatively flat remain well above basic operating costs. The rate of the US Gulf-Europe route has decreased by 4.6% to $8,233/day. The rate of the Black Sea to Far East route has fallen by 3.2% to $8,394/day. In addition, the rate of the Europe-Far East route has fallen by 5.1% to $10,050/day. The cost to charter a supramax vessel for an Asia-NOPAC or Australian round-trip voyage has declined by 1.7% to $7,413/day. In the time charter market, the supramax time charter market was not at all active last week. No supramax vessels were chartered for period deals last week. In comparison, the previous week saw one supramax vessel chartered for a period deal.

HEADLINES

- Do shipping markets want Biden or Trump for the win?

- All 18 crew safe after fire on Japanese-owned tanker off Singapore

- Singapore launching $44m co-investment initiative for maritime tech start-ups

- Cosco debuts Global Shipping Industry Chain Cooperation Initiative

- US warns of more shipping sanctions

- China continues seaport consolidation as Dalian offer goes unconditional