Expert says no visible upward drivers on the bunker market at the moment

World fuel indexes have demonstrated downward evolution during the week, still been pressured by evidences of an ongoing fuel glut despite efforts led by OPEC to tighten the market by holding back production. The underlying factors for the price drop are the same as before: U.S. shale production continues to rise; inventories remain elevated; and the markets are concerned that the OPEC cuts are not doing enough to drain the surplus.

MABUX World Bunker Index (consists of a range of prices for 380 HSFO, 180 HSFO and MGO at the main world hubs) also continued downward movement in the period of Jun. 08 – Jun.15:

380 HSFO – down from 282.50 to 279.43 USD/MT (-3.07)

180 HSFO – down from 321.86 to 319,79 USD/MT (-2.07)

MGO – down from 482.07 to 474.00 USD/MT (-8.07)

Major Banks have started lowering their oil price forecasts for this year and next. Goldman Sachs cut its Brent price forecast for this year to US$55.39 per barrel (minus US$1.37). It also revised down its WTI projections to US$52.92 a barrel (minus US$1.88). As per Goldman, the oil glut will return after OPEC’s deal expires.

For 2018, it was JP Morgan that made the most drastic cut to its oil price projections, expecting failure of OPEC cut production deal. JP Morgan slashed its 2018 WTI forecast by US$11 to US$42, and for Brent by US$10 to US$45. Bank considers that the 2018 oil market balance now points to rapid builds in inventories which, absent continued OPEC support, should depress oil and fuel prices. On the other hand, U.S. crude output is expected to keep growing for several quarters due to lower breakeven costs and higher investment. The main conclusion is: if OPEC wants to keep the market balanced next year, they will probably need to extend the production cut to all of 2018.

The EIA stated that the massive inventory overhang might last longer than it origi-nally predicted. It is also growing more confident that U.S. oil production will surge past 10 million barrels per day (mb/d) by 2018 (would be an all-time record for the United States). The EIA also expects relatively unimpressive drawdowns in inventories this year, projecting declines of just 0.2 mb/d worldwide in 2017. But the most pessimistic point is that the EIA sees inventories rising again in 2018 by 0.1 mb/d.

Saudi Arabia in turn predicts that crude markets will rebalance despite of U.S. companies’ drilling activity rises. The country doesn’t see any need for changes to the oil-cuts deal agreed on by OPEC and its allies last month in Vienna. At the same time, Russia is committed to doing everything it can to balance the market. It forecasts, that a deal among oil-producing countries to curb production and balance an oversupplied market will achieve its objective in the first quarter of next year.

Nevertheless, a 10-percent decline in oil prices since late May could push traders to keep crude in storage. Shipping data shows that at least 15 supertankers are still staying in Southeast Asia’s Strait of Malacca and Singapore Strait, filled with unsold fuel. While that is less than in previous months, it’s still very possible that volumes in storage could easily rise. 21.5 million barrels per day (mb/d) of crude came to Asia on tankers in May (down from a peak in February, but similar to levels in late 2016, before production cuts were announced).

The severing of diplomatic ties by several Gulf States with Qatar became a move that temporarily rattled the fuel market. The initial reaction was that any tension in the Middle East is always supportive for crude and fuel. However, major effect of this diplomatic confrontation is likely to be felt in the shipping sector. Ships traveling to and from Qatar have to find an alternate refueling port, and LNG shippers will have to adjust schedules and routes. This will increase costs, and in the near term, may form some support to the fuel prices.

Nigeria has presented downside risks to fuel prices. On Jun.06 Royal Dutch Shell just lifted its force majeure on its Forcados oil shipments (an estimated 250,000 barrels per day) which has been offline for more than a year. It means that Nigeria is set to add the equivalent of one-fifth of the size of the OPEC cuts back into the market. Libya also revived output to 820,000 barrels a day, from 618,000 last week, after restarting its Sharara oilfield.

Threatening to undermine OPEC’s efforts is rising U.S. drilling activity, which has driven up output in the United States by more than 10 percent since mid-2016, to over 9.3 million bpd. American explorers added oil rigs for the 21st straight week to the highest level since April 2015: by 8 to 741 units. Meantime, U.S. exports have spiked in recent weeks. However, higher levels of U.S. exports do not necessarily mean global fuel market is rebalancing: U.S. producers are simply taking advantage of temporary pricing differentials (Brent-WTI).

China’s crude imports increased as well (averaged about 8.8 million barrels a day in May, up 4.8 percent from the previous month) as refiners snatched up cargoes to prepare for the end of seasonal maintenance. Net exports of oil products jumped 50 percent from April to 1.51 million tons. Crude demand has increased on growing need for transportation fuels and strategic stockpiling. Meanwhile, domestic output has stagnated as producers shut high-cost wells.

Taken altogether, the fundamentals continue to look poor. The end result could be that oil indexes may get stuck in the mid-$40s in the near run, rather than gradually rising as pre-viously expected. There are no visible upward drivers on the bunker market at the moment. We expect bunker prices may continue downward evolution next week.

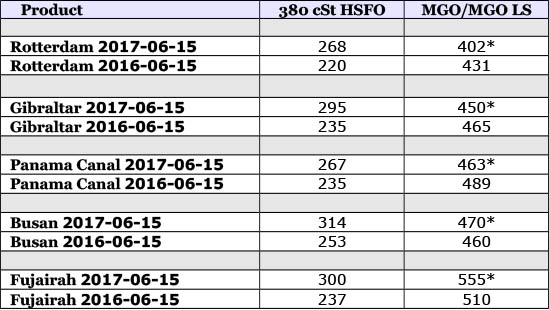

* MGO LS

All prices stated in USD / Mton

All time high Brent = $147.50 (July 11, 2008)

All time high Light crude (WTI) = $147.27 (July 11, 2008)

Source: Marine Bunker Exchange

HEADLINES

- Do shipping markets want Biden or Trump for the win?

- All 18 crew safe after fire on Japanese-owned tanker off Singapore

- Singapore launching $44m co-investment initiative for maritime tech start-ups

- Cosco debuts Global Shipping Industry Chain Cooperation Initiative

- US warns of more shipping sanctions

- China continues seaport consolidation as Dalian offer goes unconditional