Liner Review…Please Sir, Not More Of The Same?

In the famous novel a young Oliver Twist pleads in vain with Mr Bumble at the workhouse “Please Sir, I Want Some More”. In early 2014, containership owners would have been looking for the opposite of the young Oliver – anything but more of the prevailing conditions. Yet once again challenging markets prevailed, and by the end of the year boxship players had probably “had enough”.

Anything But More

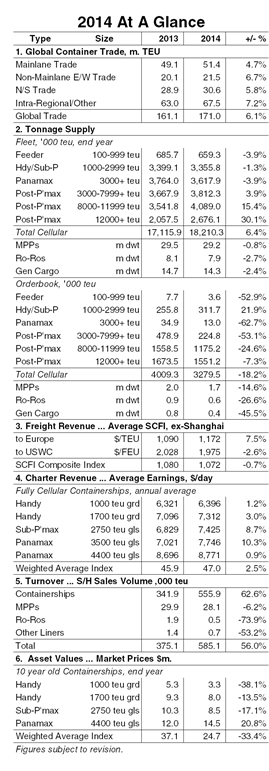

After five years in the doldrums, 2014 was essentially more of the same for the liner sector. With the global economic downturn having cut harder into  demand in the box sector than almost anywhere else, half a decade on and containership operators were still found wrestling with the need to find ways to absorb potentially surplus capacity. The fully cellular containership fleet expanded by around 6% to 18.2m TEU in full year 2014, and trade growth in the same ballpark was not enough to push the market balance back into a more positive direction.

demand in the box sector than almost anywhere else, half a decade on and containership operators were still found wrestling with the need to find ways to absorb potentially surplus capacity. The fully cellular containership fleet expanded by around 6% to 18.2m TEU in full year 2014, and trade growth in the same ballpark was not enough to push the market balance back into a more positive direction.

Fed Up Yet?

Box freight market conditions remained extremely volatile with liner companies in an ongoing battle to manage incoming capacity. Average spot freight rates for the year were up a little (7%) on the Far East-Europe route but down a little (3%) on the Transpacific. Few liner companies (except the market leader) made substantial profits, although towards the end of the year falling bunker prices at least started to reduce liner company costs.

If anything, the story was even worse on the charter market. Earnings remained depressed for yet another year, with only limited gains on historically low levels. Cascading of capacity from the mainlanes, allied to idle capacity, kept the pressure on charter owners, although later in the year there was some relief in the Panamax sector where unexpectedly robust redeployment onto intra-regional trades and a declining fleet provided more substantial support for rate levels than in other size sectors. Panamaxes also bucked the trend against generally falling asset prices in the boxship sector, with end year 10 year old secondhand prices up over 20% on end 2013 levels.

Ready For A New Twist?

So, if everyone has “had enough” and can’t take any “more”, what might change? Well, the industry consensus suggest things are getting a little tighter now. Plenty of capacity has been absorbed by slow steaming (with no sign yet of lower bunker prices changing things, though this needs to be watched carefully), much less capacity is idle (around 1.3% of the total fleet today) than in previous winters and the orderbook looks much more manageable at 18% of the fleet. Demolition remains historically high, with 0.4m TEU scrapped in 2014. Meanwhile, port congestion, most obviously on the US West Coast, may start to soak up significant amounts of capacity.

More And More

This might be enough to convince some investors that there’s no more (pain) to come and it’s time for a change in fortunes. But at the same time, liner companies still have plenty of big ships scheduled for delivery (and look set for another spending spree, placing orders for a new wave of ships of 20,000 TEU and above). Whatever the view of the optimists, extra capacity to be added, allied to economic headwinds in a number of parts of the world, will certainly pose challenges for the sector. Containership market players will have to artfully dodge the obstacles if they don’t want to be asking why they have had more of the same this time next year. Wish them luck. Have a nice day.

HEADLINES

- Reversal! HMM Union Drops Opposition, Headquarters Relocation to Busan Confirmed

- Five Major Shipping Lines Have Over 30 Vessels Trapped in the Strait of Hormuz

- COSCO SHIPPING Holdings Achieves RMB 5.877 Billion in Net Profit Attributable to Parent Company in Q1 2026

- VLCC Idle Rate Climbs to 55%! Tanker Owners Grapple with Scarcity of Physical Cargoes

- COSCO SHIPPING Energy: Acquires 100% Equity of Dalian Investment; Q1 Net Profit Soars by 206.7%

- China's largest domestically built LNG carrier delivered