MABUX: High volatility on bunker market before the meeting in Algiers

World fuel indexes have not had any firm trend during the week while the main supportive factor on the market was still speculation that OPEC talks in the end of September together with non-OPEC producers could result in a crude output freeze.

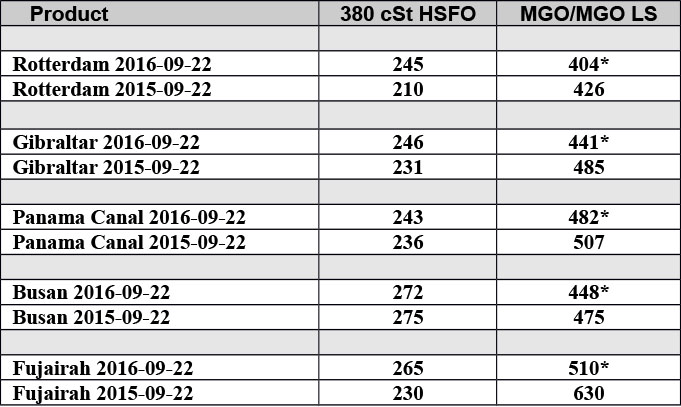

MABUX World Bunker Index (consists of a range of prices for 380 HSFO, 180 HSFO and MGO at the main world hubs) has not demonstrated any directed movement and finally only slightly rose in the period of Sep.15-22:

380 HSFO – up from 237.14 to 242.07 USD/MT (+4,93)

180 HSFO – up from 279.07 to 284.86 USD/MT (+5,79)

MGO – up from 465.50 to 471.64 USD/MT (+6,14)

U.S. crude stockpiles fell 6.2 million barrels to 504.6 million in the week ended Sept. 16. Stockpiles remain at the highest seasonal level in more than 20 years. Crude imports rose 3.1 percent to 8.31 million barrels a day last week. Production increased 0.2 percent to 8.51 million barrels a day. Refineries cut operating rates by 0.9 percentage point to 92 percent of capacity, the lowest level since June.

Due to some weak economic numbers in the U.S. the chances of a rate hike seem to be diminishing in September and Fed will probably push it out to December. Last week economic indicators pointed to uneven growth in the U.S., while sliding oil prices and a selloff in banks also contributing to losses.

OPEC may turn its planned informal meeting in Algiers next week into a formal session as it seeks ways with other producers to cut crude supplies by 1 million barrels a day to rebalance markets and stabilize prices. As per OPEC’s evaluation, oil needs another six to nine months to stabilize within a range of $50 to $60 a barrel. Cartel must reach an equitable agreement that all its members support, and any accord must also satisfy non-OPEC producers. Meantime, OPEC probably won’t clinch a deal as members stay focused on either boosting output or defending their market share. Iran and Iraq have signaled their resolve to increase output, while group leader Saudi Arabia is maintaining near-record supply. The kingdom denied there was any current need to cap production and is reluctant to constrain output as the resulting boost for prices could revive supplies from U.S. shale drillers. The IEA said before, the surplus in global oil markets will last for longer than previously thought, persisting into late 2017 as demand growth slumps and supply proves resilient.

In case of a freeze success it would be the group’s first decision to limit output since OPEC adopted a Saudi-led plan in 2014 allowing members to pump more to protect market share from increased production from the U.S. and Russia. OPEC members and Russia failed to agree at a meeting in Doha in April to limit production after Iran declined to attend and Saudi Arabia refused to proceed without all of the OPEC states participating.

Venezuela is the most active supporter to the possible freeze deal. As per Venezuelan President Nicolas Maduro, members are close to reaching an agreement. Venezuela’s evaluation is that global production is at 94 million barrels per day, of which market needs to go down 9 million barrels per day to sustain the level of consumption. The statements came the same day as credit ratings agency Standard & Poor’s said that a proposed bond swap by PDVSA was a distressed exchange which may destroy effort to seek a financial lifeline.

Market concerns are growing over the possibility of returning crude supplies from Libya and Nigeria, that are looking to resume some facilities in the coming weeks. Libya’s state oil company lifted curbs on crude sales from the ports of Ras Lanuf, Es Sider and Zueitina, potentially unlocking 300,000 barrels a day of supply. In total the resumption of shipments from the three Libyan ports would allow Libya to double crude output to 600,000 barrels a day within four weeks. As a first step, a tanker Seadelta sailed from Libian port of Ras Lanuf on Sep.21 with 781,000 barrels of crude. Another tanker, the Syra, is going to ship another 600,000 barrels of crude to Italy from Ras Lanuf to Italy soon.

Nigeria’s output reached 1.75 million barrels a day and will keep rising after government out-reach and a cease-fire with militants allowed some production to restart. It is also expected that Nigerian production should reach 1.8 million barrels a day next month and 2 million by December, when most export terminals resume operations. The nation’s output fell in May to the lowest in 27 years after increasing attacks by militants on oil infrastructure and was at 1.44 million barrels a day in August.

An increase in shipments from the African countries would negate the influence a production freeze would have on the market. If OPEC members agree to a freeze and some countries are bringing back production the market will come under noticeable pressure again.

China and India have used low oil prices to shore up their Strategic Petroleum Reserves (SPR). However, as China doesn’t report its storage regularly, the data and the expectations of the experts are skewed. While one forecast (JP Morgan) believes that the Chinese are close to topping up their SPR, another one (Energy Aspects) believes that new commercial storage capacity additions will sustain the increased demand from China. The difference between the two possibilities accounts for a huge difference of 1.1 million barrels a day. Nevertheless, with reports of a likely debt crisis or a hard landing in China, chances are that the oil demand from the world’s second-largest economy will remain flat or see muted growth in 2017.

We expect high volatility on the global fuel market before the meeting of major oil-producing nations in Algiers on Sep.26-28. Bunker prices may demonstrate irregular fluctuations next week with no firm trend.

* MGO LS

All prices stated in USD / Mton

All time high Brent = $147.50 (July 11, 2008)

All time high Light crude (WTI) = $147.27 (July 11, 2008)

HEADLINES

- Reversal! HMM Union Drops Opposition, Headquarters Relocation to Busan Confirmed

- Five Major Shipping Lines Have Over 30 Vessels Trapped in the Strait of Hormuz

- COSCO SHIPPING Holdings Achieves RMB 5.877 Billion in Net Profit Attributable to Parent Company in Q1 2026

- VLCC Idle Rate Climbs to 55%! Tanker Owners Grapple with Scarcity of Physical Cargoes

- COSCO SHIPPING Energy: Acquires 100% Equity of Dalian Investment; Q1 Net Profit Soars by 206.7%

- China's largest domestically built LNG carrier delivered