Global chem shipping problem to persist for years

The too-many-ships problem is not going away anytime soon, at least for the chemical tanker fleet.

London-based maritime consultant Drewry said in a report issued on Thursday that freight rates on long-haul routes will continue to be challenged by a surplus of large vessels over the next two years.

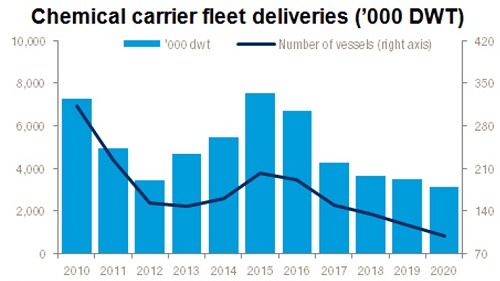

“The chemical fleet grew by 5.2% in 2016 and is expected to expand by 3.3% to the end of 2017, which will continue squeezing rates on major routes over the next two years,” said Hu Qing, Drewry’s lead analyst for chemical shipping.

“New orders and deliveries are also expected to decline further because of the depressed market and financial woes of shipyards.”

Source: Drewry’s Chemical Forecaster

Too many ships chasing too few cargoes has plagued chemical shipping off and on for years, and this dilemma is expected to continue.

Drewry’s Chemical Forecaster study used similar language in late 2016, stating that rising fleet growth and softening seaborne trade will depress chemical shipping freight rates over the next few years.

Chemical shipper Stolt Nielsen has referred often to the problem in earnings reports over the past few years and did so recently.

“There is still an oversupply of tonnage, and with significant new building deliveries in 2017, combined with a weak product tanker market, we believe the year will be challenging,” said CEO Niels G Stolt-Nielsen.

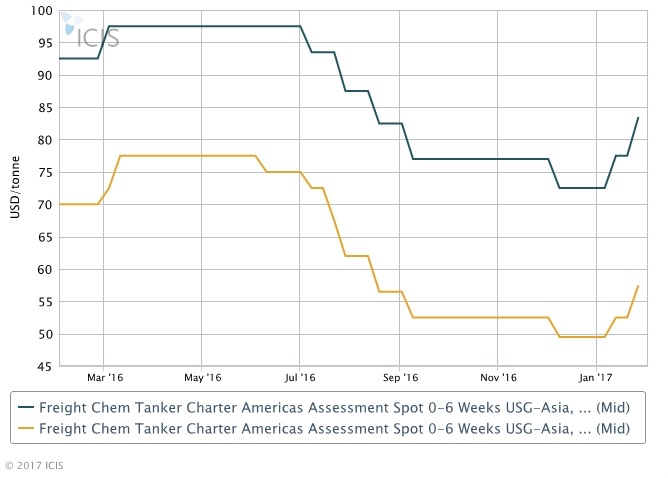

Freight rates on the two major chemical shipping routes in the Americas – the transatlantic eastbound and the US Gulf to Asia trade lane – declined by 9% during 2016, though some rates turned up in January this year. The chart below shows rates for 2,000-tonne shipments in blue and 5,000 tonnes in gold.

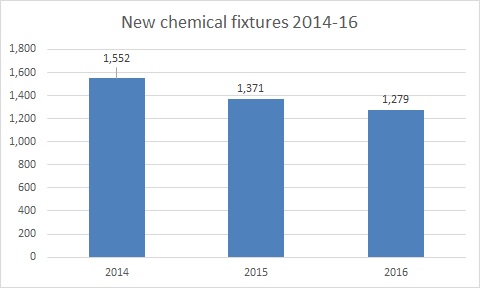

New fixtures reported in the ICIS shipping report last year declined by 7% from 2015.

Source: ICIS Weekly Chemical Tanker Shipping Report

There has been a surplus of chemical shipping vessel supply on major routes, with many new building deliveries and swing tankers flooding the market, said Drewry’s latest report.

Time charter rates weakened in 2016, especially for larger tankers, and freight rates on major long-haul routes dropped. While trade volume from the US to Europe and northeast Asia surged in 2016, the addition of speculative vessels brought rates down.

The chemical fleet will continue to expand because of the large number of new vessel orders placed in previous years, but growth will be subdued compared to 2015-2016, Drewry said.

While deliveries and ordering have declined in 2016, there are still many ships scheduled to be delivered in the next five years because of heavy ordering during 2014 and 2015.

More demolitions are expected because of new regulations that will come into force in 2017.

Coupled with the implementation of the Ballast Water Treatment System (BWTS) in September 2017, the adoption of the global 0.5% sulphur cap may potentially accelerate the rate of vessel demolition towards the end of 2020.

However, this is likely to have little impact on fleet supply, as most of the older ships are of less than 10,000 dwt (deadweight tonnes), and thus, the capacity that can be scrapped will be a small percentage of the total fleet.

Time charter rates weakened further in the fourth quarter of 2016, more so for larger tankers.

“We expect fleet oversupply to persist in 2017 and time charter rates for larger ships, especially MRs [medium ranges], to decline because of stiff competition. However, rates for vessels in the smaller categories are likely to remain stable in 2017,” said the Drewry analyst.

Source: ICIS (By Lane Kelley)

HEADLINES

- Do shipping markets want Biden or Trump for the win?

- All 18 crew safe after fire on Japanese-owned tanker off Singapore

- Singapore launching $44m co-investment initiative for maritime tech start-ups

- Cosco debuts Global Shipping Industry Chain Cooperation Initiative

- US warns of more shipping sanctions

- China continues seaport consolidation as Dalian offer goes unconditional