Charting The Consolidation Of Container Shipping

Last year saw a huge amount of change in the under pressure container shipping sector. In particular, the ongoing consolidation of the sector in one form or another grabbed the headlines. To put this into context, it’s interesting to see how the level of consolidation relates to other parts of shipping, how it has developed over time and how it might progress looking forward.

Solid In A Fragmented Field

It’s quite clear that the shipping industry is a fairly fragmented business. On the basis of start 2017 Clarksons Research data, 88,892 ships in the world fleet were spread across 24,267 owners. That works out at less than 4 vessels per owner. Although 145 owners with more than 50 ships accounted for almost 12,000 of the vessels (and 29% of the GT), it’s still not that consolidated. The liner shipping business however is one the more consolidated parts of shipping, as well as being home to some of the industry’s larger corporates. At the start of the year, the 5,154 containerships in the fleet were owned by 622 owner groups, about 8 ships per owner, but, perhaps more pertinently, were operated by 326 carriers, about 16 ships per operator. Each of the top 8 operators deployed more than 100 ships. But despite the less fragmented nature of the sector, recent market conditions have led to another round of consolidation in the box business.

It’s quite clear that the shipping industry is a fairly fragmented business. On the basis of start 2017 Clarksons Research data, 88,892 ships in the world fleet were spread across 24,267 owners. That works out at less than 4 vessels per owner. Although 145 owners with more than 50 ships accounted for almost 12,000 of the vessels (and 29% of the GT), it’s still not that consolidated. The liner shipping business however is one the more consolidated parts of shipping, as well as being home to some of the industry’s larger corporates. At the start of the year, the 5,154 containerships in the fleet were owned by 622 owner groups, about 8 ships per owner, but, perhaps more pertinently, were operated by 326 carriers, about 16 ships per operator. Each of the top 8 operators deployed more than 100 ships. But despite the less fragmented nature of the sector, recent market conditions have led to another round of consolidation in the box business.

All Change At The Big End

The three largest operators (by deployed capacity) at the start of 2017 were European: Maersk Line (647 vessels deployed) followed by MSC (453) and CMA-CGM (454). Of the remaining carriers in the top 20 all but three were based in Asia or the Middle East. However, what’s really interesting is that out of the 20 largest carriers back in late 2014, 4 are now gone. CSAV was acquired by Hapag-Lloyd, NOL/APL by CMA-CGM and the two major Chinese lines merged. And of course in late summer 2016, the financial collapse of Hanjin Shipping marked the sector’s biggest casualty in 30 years.

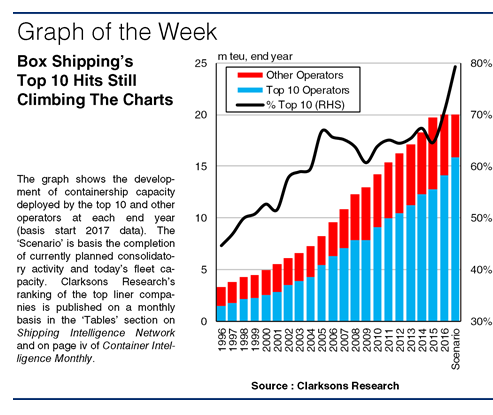

Long-Term Liner Trends

Against this backdrop, the graph shows that the latest wave of box sector consolidation is actually part of a long-term trend. Back in 1996 the top 10 carriers deployed 45% of capacity and at the start of 2017 that figure stood at 70%. The coming year is set to see Hapag-Lloyd complete its merger with UASC, and Maersk Line’s planned acquisition of Hamburg-Sud is also awaiting necessary approvals. The second half of last year also saw the three major Japanese operators declare their intention to merge containership operations in a joint venture due to be established this year and start operations in 2018. The ‘scenario’ based on these changes would see the top 10’s share at 79%, nearly twice as much as 20 years ago.

Tracking The Top Table

So, the container sector is one of the more consolidated parts of shipping, and both the long-term trend and recent developments point towards ongoing consolidation. Many hope this will help the recalibration of market fundamentals and eventually support improved conditions. In the meantime, we’ll be publishing the ranking of the top containership operators every month, so watch this space.

Source: Clarksons

HEADLINES

- Reversal! HMM Union Drops Opposition, Headquarters Relocation to Busan Confirmed

- Five Major Shipping Lines Have Over 30 Vessels Trapped in the Strait of Hormuz

- COSCO SHIPPING Holdings Achieves RMB 5.877 Billion in Net Profit Attributable to Parent Company in Q1 2026

- VLCC Idle Rate Climbs to 55%! Tanker Owners Grapple with Scarcity of Physical Cargoes

- COSCO SHIPPING Energy: Acquires 100% Equity of Dalian Investment; Q1 Net Profit Soars by 206.7%

- China's largest domestically built LNG carrier delivered