The Offshore Markets: 2016 In Review

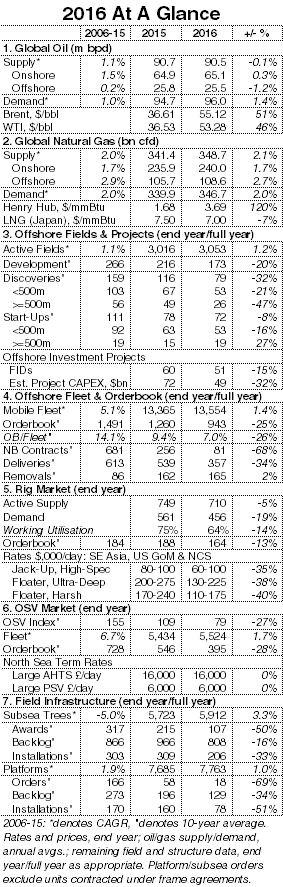

Expectations at the start of the year that 2016 would be a tough one for the oil industry, and in particular for offshore, were on the whole fulfilled. Overall upstream E&P spending globally fell for the second successive year, and was down by in the region of 27% year-on-year in 2016. Cost-cutting has been a key focus, whether that be through pressure on the supply chain, M&A activity, job cuts or other means.

Lower Spending

Offshore spending has been particularly reined back on exploration activity such as seismic survey and exploration drilling, although 2016 saw weakness spread further to areas such as the subsea or mobile production sectors which had initially shown some degree of protection from the downturn. This was not helped by a 32% year-on-year decline in sanctioned offshore project CAPEX in 2016, despite a small number of encouraging project FIDs, such as that for Mad Dog Phase 2 in the Gulf of Mexico in Q4.

Dayrate Weakness

Dayrates and asset values in those offshore sectors with liquid markets showed further signs of weakening in 2016. Clarksons Research’s index of global OSV termcharter rates declined by 27% in 2016, whilst that for drilling rigs was down by 25% year-on-year. Potential for further falls are, in general, limited, given that rates levels in many regions are close to operating expenses. Owners are doing what they can to control the supply side: just 81 offshore orders were recorded in 2016: for context, more than 1,000 offshore vessels were ordered at the height of the 2007 boom. Slippage has also remained evident, either due to mutually agreed delays with shipyards, or owing to owners cancelling orders. Offshore deliveries were 34% lower y-o-y in 2016.

Despite the severe industry downturn, the oil price actually firmed during the year. Brent crude began 2016 at $37/bbl, before briefly dipping below $30/bbl. However, the price ended 2016 at $55/bbl, helped by a slow firming in mid-year, and then more rapid gains after the 30th November announcement of a concerted oil production cut by OPEC countries.

This is clearly positive news for oil companies’ cashflow, and marks the abandoning of Saudi Arabia’s policy of targeting market share by accepting low prices as a means to hinder shale oil production in the US. However, US onshore companies were already feeling more comfortable with slightly improved prices in Q3 2016. Early surveys of intentions for E&P spending suggest that onshore spending in the US could increase by more than 20% in 2017. It is likely that offshore spending will decline further in 2017.

Some Way To Go

Nonetheless, it is important to stress that the offshore sector is far from dead. The expected multi-year downturn is occurring. However, important cost-control and consolidation has taken place. IOCs continue to consider strategic investments such as Coral FLNG or Bonga Lite. This shows that these companies are planning for better times. Decline at legacy fields will help to correct the supply/demand balance. Meanwhile, optimism is building in the renewables and decommissioning markets, with for example, announcements even in the first few days of 2017 that China is to make an RMB2.5 trillion investment in renewables over five years, whilst another North Sea decommissioning project plan has been submitted.

Nevertheless, the supply/demand imbalance in many offshore vessel sectors will take time to recalibrate. However, the weakness of 2016 also put in place many longer term trends which could lay the groundwork for an eventual change in market fortunes.

Source: Clarksons

HEADLINES

- Do shipping markets want Biden or Trump for the win?

- All 18 crew safe after fire on Japanese-owned tanker off Singapore

- Singapore launching $44m co-investment initiative for maritime tech start-ups

- Cosco debuts Global Shipping Industry Chain Cooperation Initiative

- US warns of more shipping sanctions

- China continues seaport consolidation as Dalian offer goes unconditional