In The Middle Of A (Supply) Chain Reaction?

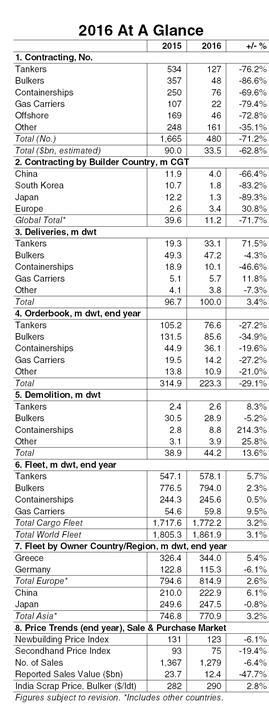

In 2016 the shipping industry saw significant supply side adjustments in reaction to continued market pressures. For shipbuilders this meant a historically low level of newbuild demand with fewer than 500 orders reported in 2016, and the volume of tonnage on order declined sharply. Meanwhile, higher levels of delivery slippage and strong demolition saw fleet growth fall to its lowest level in over a decade.

Pressure Building Up

2016 was an extremely challenging year for the shipbuilding industry. Contracting activity fell to its lowest level in over 20 years with just 480 orders reported, down 71% year-on-year. Domestic ordering proved important for many builder nations and 68% of orders in dwt terms reported at the top three shipbuilding nations were placed by domestic owners last year. Despite a 6% decline in newbuild price levels over 2016, few owners were tempted to order new ships, especially with the secondhand market offering ‘attractive’ opportunities. Only 48 bulkers and 46 offshore units were reported contracted globally last year, both record lows, and tanker and boxship ordering was limited. As a result, just 126 yards were reported to have won an order (1,000+ GT) in 2016, over 100 yards fewer than in 2015.

A Spot Of Relief

However, a record level of cruise ship and ferry ordering provided some positivity in 2016. Combined, these ship sectors accounted for 52% of last year’s $33.5bn estimated contract investment. European shipyards were clear beneficiaries, taking 3.4m CGT of orders in 2016, the second largest volume of orders behind Chinese shipbuilders’ 4.0m CGT. Year-on-year, contracting at European yards increased 31% in 2016 in terms of CGT while yards in China, Korea and Japan saw contract volumes fall by up to 90% year-on-year.

Further Down The Chain

In light of such weak ordering activity, the global orderbook declined by 29% over the course of 2016, reaching a 12 year low of 223.3m dwt at the start of January 2017. This is equivalent to 12% of the current world fleet. The number of yards reported to have a vessel of 1,000 GT or above on order has fallen from 931 yards back at the start of 2009 to a current total of 372 shipbuilders.

Final Link In The Chain

Adjustments to the supply side in response to challenging market conditions in 2016 have also been reflected in a slower pace of fleet growth. The world fleet currently totals 1,861.9m dwt, over 50% larger than at the start of 2009, but its growth rate slowed to 3.1% year-on-year in 2016. This compares to a CAGR of 5.9% between 2007 and 2016 and is the lowest pace of fleet expansion in over a decade. A significant uptick in the ‘non-delivery’ of the scheduled start year orderbook in 2016, rising to 41% in dwt terms, saw shipyard deliveries remain steady year-on-year at a reported 100.0m dwt. Further, strong demolition activity helped curb fleet growth in 2016 with 44.2m dwt reported sold for recycling, an increase of 14% year-on-year.

End Of The Chain?

So it seems that the ‘market mechanism’ has finally been kicking into action. A more modest pace of supply growth might be welcome news to the shipping industry but further down the chain shipbuilders are suffering. Contracting levels plummeted in 2016 and the orderbook is now significantly smaller. Even with the ongoing reductions in yard capacity, shipbuilders worldwide remain under severe pressure and will certainly be hoping for a more helpful reaction in 2017.

Source: Clarksons Research

HEADLINES

- Reversal! HMM Union Drops Opposition, Headquarters Relocation to Busan Confirmed

- Five Major Shipping Lines Have Over 30 Vessels Trapped in the Strait of Hormuz

- COSCO SHIPPING Holdings Achieves RMB 5.877 Billion in Net Profit Attributable to Parent Company in Q1 2026

- VLCC Idle Rate Climbs to 55%! Tanker Owners Grapple with Scarcity of Physical Cargoes

- COSCO SHIPPING Energy: Acquires 100% Equity of Dalian Investment; Q1 Net Profit Soars by 206.7%

- China's largest domestically built LNG carrier delivered