MABUX: High level of uncertainty prevails in the global bunker market

World fuel indexes dropped to their lowest levels since December during the week when the optimism surrounding the OPEC deal was just getting underway, but turned into upward correction recently as U.S. crude stockpiles unexpectedly decline last week. The market’s volatility surged the most since before the 2014 price crash started.

MABUX World Bunker Index (consists of a range of prices for 380 HSFO, 180 HSFO and MGO at the main world hubs) dropped in the period of Mar.09 – Mar.16:

380 HSFO – down from 297.07 to 283.00 USD/MT (-14,07)

180 HSFO – down from 339.36 to 326.21 USD/MT (-13,15)

MGO – down from 517.21 to 510.07 USD/MT (-7,14)

OPEC’s strategy to balance the oil market and bolster prices is facing its biggest test now. The producer group is aiming to revamp the market by eroding a crude inventory surplus that’s depressed prices since 2014. However, a deal to cut output had the side-effect of triggering a surge in U.S. production and a jump in the inventories to an all-time high. So at the moment the effect of the cuts looks much more short-lived than expected, and the fall in prices last week may indicate a kind of turning point.

OPEC’s February report showed total output had fallen from 32.097 million bpd in January to 31.958 million bpd. Members which agreed to the production freeze and cuts were able to reduce production from 29.9 million to 29.7 million bpd.

The International Energy Agency in turn estimated OPEC compliance with agreed output cuts at 98% in the first two months of the year, while Saudi compliance was at 135%. At the same time Russia and other non-OPEC producers’ adherence to agreed cuts in the period was only at 37%. If current output levels maintained to June the IEA sees an implied market deficit of 500,000 b/d in the first half of 2017.

Though OPEC has managed to achieve a high standard of compliance, it has mostly been due to the oversized cut by the largest member of the group—Saudi Arabia. However, last week Saudi Arabia let it leak that the kingdom has no intention of leading OPEC toward another cut in production to accommodate the growing volumes of oil from American shale deposits. It is quite possible that if the situation doesn’t improve in the next few weeks, it is unlikely that Saudi Arabia will continue to bear the responsibility alone.

Besides, two OPEC members, Iran and Iraq, are weakening Saudi Arabia’s position by taking steps to boost production. According to the IEA, Iraq will increase its output to 5.4 million barrels per day by 2022, which is significantly higher than the earlier estimates of an increase to 4.6 million bpd by 2021. Similarly, Iran is expected to boost production by 400,000 bpd to reach 4.15 million bpd production in 2022.

A kind of price supporting factor at the moment is Libya, where oil output has allegedly dropped by about 80,000 barrels a day since clashes broke out. Output is now around 620,000 barrels per day (far less than the 1.6 million barrels a day it produced before a 2011 uprising) as Es Sider, the country’s biggest oil port, and Ras Lanuf, its third-largest, remain closed. The country’s state oil company – NOC – stated that the Company could declare state of force majeure if the current clashes continue for long.

The fact that U.S. crude inventories are breaking records every week and oil prices have failed to post any gains so far in 2017 offers the evidence that the comeback in the U.S. oil industry is undermining the effectiveness of the OPEC deal. The U.S. shale oil drillers have used higher prices to add new rigs for the past eight weeks in a row. In the week to March 10, the total rig count increased to 617, compared to 386 a year ago. Though the rig count is still way below the peak of 1,609 reached in October 2014, the recovery from the six-year lows of 316 rigs in May 2016, has been outstanding.

As a result, U.S. crude oil production, which had dropped from the highs of 9,600,000 bpd in June 2015, to a low of 8,428,000 bpd in July, 2016 is on the rise once again. In the week ending March 10, 2017, U.S. crude output rose for a fourth week, advancing 21,000 barrels a day to 9.11 million barrel a day, the highest level since February 2016. The worrying part for OPEC is that the EIA estimates that U.S. oil production will average 9,210,000 bpd this year.

The U.S. Federal Reserve raised interest rates by 25 basis points to a range of 0.75 percent to 1.00 percent for the second time in three months. The decision was spurred by steady economic growth, strong job gains and confidence that inflation is rising to the central bank’s target: the arguments supporting global fuel prices as well.

What happens next is uncertain. The much faster return of U.S. shale production and soft fuel prices have stimulated discussions within OPEC to extend the six-month deal until the end of the year. This week Kuwait became the first member to officially endorse a roll-over of the production cuts for another six months. Iraq and Angola have also suggested they would be open to an extension. It is obvious that fuel indexes will drop if OPEC says that they are not open to extending their production cuts. On the other hand, if prices remain low, OPEC only stands to lose market share to its competitors by continuing the production cuts.

We do not expect that the situation on the bunker market will clear up next week too much. So bunker prices may stay rather volatile and continue to demonstrate irregular changes.

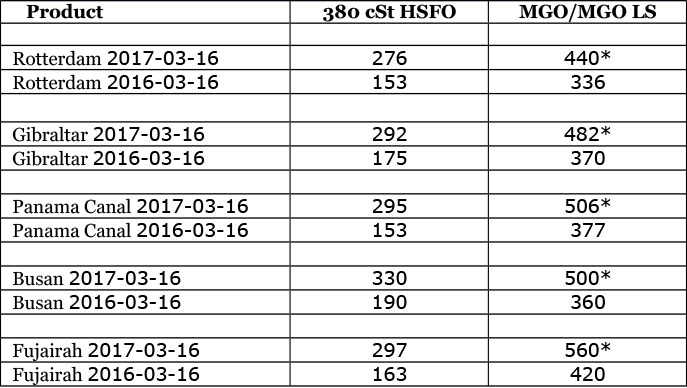

* MGO LS

All prices stated in USD / Mton

All time high Brent = $147.50 (July 11, 2008)

All time high Light crude (WTI) = $147.27 (July 11, 2008)

Source: Marine Bunker Exchange

HEADLINES

- Dual-Fuel Fleet Surges to 400 Ships as Alternative-Fuel Investment Defies Market Slowdown

- Do shipping markets want Biden or Trump for the win?

- All 18 crew safe after fire on Japanese-owned tanker off Singapore

- Singapore launching $44m co-investment initiative for maritime tech start-ups

- Cosco debuts Global Shipping Industry Chain Cooperation Initiative

- US warns of more shipping sanctions