World’s bunker market still in waiting mood, expert says

The Easter holiday break shut many markets for as long as four days this week and so has not given any chance for world fuel indexes to set up the firm trend: they were changing insignificant and irregular. Still the speculation that the Organization of Petroleum Exporting Countries and its allies will extend their six-month pact aimed at eroding a global glut is helping boost prices, while there is also concern that rising U.S. output will counter the reductions.

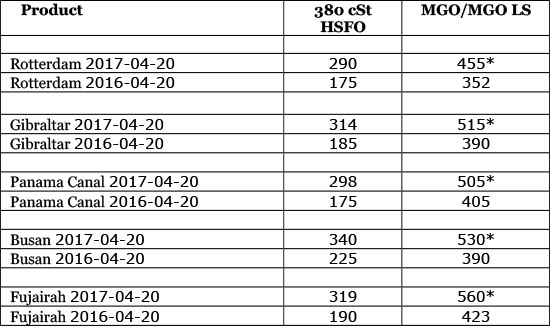

MABUX World Bunker Index (consists of a range of prices for 380 HSFO, 180 HSFO and MGO at the main world hubs) has decreased slightly in the period of Apr. 13 – Apr. 20:

380 HSFO – down from 306.36 to 299.21 USD/MT (-7.15)

180 HSFO – down from 347.07 to 339.14 USD/MT (-7.93)

MGO – down from 527.14 to 519.28 USD/MT (-7.86)

One of the main geopolitical worries for global fuel market is still Syria and possi-ble cancellation by Russia of its cooperation with the U.S. (and others) with regards to operational security in the area. The risk of a military confrontation between the different armed players in the conflict has increased. Several NATO countries, such as Belgium, have already postponed further air force operations in Syria.

At the same time, the Arab countries also don’t seem to be totally supporting the U.S. attack on Syria. Iraq indicated its worries while the region’s leading military and political power, Egypt, has openly criticized the military action. This in stark contrast to most of the countries from Gulf Cooperation Council (Saudi Arabia, Kuwait, the United Arab Emirates, Qatar, Bahrain, and Oman).

In the short term, the global oil market might not feel an effect of the actions in Syria. Syria’s position as an oil and gas producer is negligible. Since the start of the fights against Assad no real effects on global oil markets have been shown. Syria only produced around 25,000-33,000 bpd in 2014-2015. The future impact, however, could be rather strong, especially if there is a spill-over of the civil war to Jordan, Saudi Arabia, or Iraq.

The IEA said in its latest report that the oil market is probably already balanced, although more data is needed. Oil inventories are falling in many parts of the world and have started to decline in the OECD as well. As per report, oil stocks in the Organisa-tion for Economic Cooperation and Development industrialized countries fell by 17.2 million barrels in March, although inventories were still 300 million barrels above the five-year average. In the coming months, it is expected that more substantial inventory declines will arrive and demonstrate that the oil market is no longer oversupplied. At the same time, the IEA downgraded its oil demand growth estimate for this year from 1.4 mb/d to 1.3 mb/d.

Goldman Sachs in turn maintains its projection that oil prices will remain stable due to improvements in drilling technology that can keep a lid on prices. The invest-ment bank says that shale will also limit volatility and offers a five-year estimate on WTI at $54 per barrel.

OPEC members Saudi Arabia, Iraq and Kuwait are reportedly targeting $60 per barrel: at that price level, government finances would stabilize while it would still be low enough to prevent a resurgence of U.S. shale. However, the risk is that OPEC is underestimating the ability of shale to ramp up. Indeed U.S. shale output is already rebounding. Nevertheless, the plans from OPEC to reach $60 per barrel raise chances for an extension of the collective production cuts.

Iran, which has been exempted from the OPEC oil production cut agreement closed last November, said it is now ready to join the initiative as long as there is consensus among the cartel’s members. The remarks suggest that Iran has reached an oil output level that it is comfortable with for the time being. There are not, howev-er, any details as to how much Iran would be willing to cut off its daily output or from what monthly production level the cut will be effected. Iran produced 3.79 million barrels daily last month, down slightly from the 3.82 million bpd in February but higher than the 3.78 million barrels in January.

U.S. crude production will likely rise in the months ahead as explorers added rigs for a 13th week, capping the longest stretch of gains since 2011 and pushing fuel prices down. Rigs targeting crude rose by 11 to 683 last week, the highest level since April 2015. The number of wells drilled has more than doubled since tumbling to 316 in May.

China reported a 6.9 percent annual growth rate in the first quarter, much better than expected. It is also setting new oil import records by the month, dispelling fears that crude oil demand was slowing down. Imports hit a record high 9.21 million bar-rels per day in March, an increase of 11 percent from February. That spike is likely temporary, but China no longer appears to be the downside risk to oil prices at the moment.

Global fuel market is in a waiting mood so far. The next steps for fuel prices de-pend largely on geopolitical factors: Syria and Korean peninsula, as well as on OPEC’s further decisions. The volatility on the market remains, and bunker prices may change irregular next week.

* MGO LS

All prices stated in USD / Mton

All time high Brent = $147.50 (July 11, 2008)

All time high Light crude (WTI) = $147.27 (July 11, 2008)

Source: Marine Bunker Exchange

HEADLINES

- Do shipping markets want Biden or Trump for the win?

- All 18 crew safe after fire on Japanese-owned tanker off Singapore

- Singapore launching $44m co-investment initiative for maritime tech start-ups

- Cosco debuts Global Shipping Industry Chain Cooperation Initiative

- US warns of more shipping sanctions

- China continues seaport consolidation as Dalian offer goes unconditional