Nordic American Tankers: The Company is in a solid financial position with a strong cashflow

The first quarter of 2017 was another good period for NAT in a volatile tanker market. NAT remains financially strong and is committed to servicing its customers and shareholders well. The average daily time charter equivalents (“TCE”) earned for the first quarter were $22,700 per day per vessel as against the previous quarter of $21,600 per day per vessel. NAT took delivery of another new Suezmax tanker February 27, 2017, the Nordic Space. We now have 30 Suezmax vessels in operation.

NAT ordered, in October 2016, three Suezmax newbuildings at Samsung Shipyard for delivery in second half of 2018. 30% of the total purchase price was paid up front in cash. We expect to finance the remaining 70%, which is due upon delivery of the ships, from cash on hand and increased debt. None of these ships are pledged under the current credit facility. These three newbuildings will increase the fleet by 10% to 33 vessels, increasing dividend and earnings capacity.

On April 19, 2017, NAT declared a cash dividend of $0.20 per share for 1Q2017, payable to shareholders of record as of May 22, 2017. Payment of the dividend is expected to be on or about June 8, 2017. Our dividend policy will continue to enable us to achieve a competitive cash yield. Except for one quarter of the last nine quarters, the dividend payout ratio has been around 70%. Funds have been withheld to partly finance the vessel acquisitions over the period.

NAT has followed the same strategy for years and has well developed and very good financial control mechanisms in place.

A key part of our business model is our focus on efficiency and low costs. NAT has achieved a high Total Return[1] (profitability) for our shareholders. The average annual Total Return since 1997 is about 10%.

Nordic American Offshore (NAO) completed a follow-on offering in March 2017. NAT participated in the offering with $10m. Following the investment NAT owns 22.6% of NAO. As a consequence of the reduced holdings in NAO, NAT recorded a dilution charge (non-cash) of $2.6m in 1Q2017. NAO is operating in a challenging offshore market. NAT is a long term shareholder to reap the benefits of an improved market.

NAT has a cash break-even rate at about $11,500 per day per ship, including financial charges and G&A costs. The operating expenses for our vessels are low; about $8,400 per vessel per day. The high quality of the NAT fleet is also evidenced by our vetting statistics, i.e. inspections of our ships by our customers. In such vetting processes safety for our crew, the environment and our assets are in focus.

In the tanker sector, the NAT stock has significant liquidity, allowing investors to buy and sell shares whenever they wish.

Some observations:

NAT has paid quarterly dividends 79 times of $48.31 in aggregate per share during the period since 1997.

Net Asset Value (NAV), or the steel value of a vessel, is irrelevant when valuing NAT as a going concern.

Together with our shareholders, our customers are the most important constituency in NAT.

Adjusted Net Operating Earnings[2] (cash surplus) have been as follows: $30.5m for 1Q2017, $28.2m for 4Q2016 and $55.9m for 1Q2016.

NAT has a credit facility of $500m, maturing in December 2020. NAT is in compliance with the provisions under the credit facility.

The net debt is currently $10.2m per vessel based on a 30 vessels fleet.

We always make sure that NAT is in compliance with IMO on Ballast Water Treatment Systems and low sulphur content in bunker oil.

Financial Information

On April 19, 2017, NAT declared a cash dividend of $0.20 per share. The dividend is expected to be paid on or about June 8, 2017 to shareholders of record as of May 22, 2017. The number of NAT shares outstanding at the time of this report is 101,969,666.

Earnings per share (EPS) in 1Q2017 were -$0.03. In 4Q2016 and 1Q2016 the EPS were -$0.38 and $0.33, respectively. EPS does not take account of financial risk. Included in the EPS for 1Q2017 is a non-cash dilution charge of -$0.02 per share related to NATs reduced holdings in NAO.

The Company’s Adjusted Net Operating Earnings in 1Q2017 were $30.5m. In 4Q2016 and 1Q2016 Adjusted Net Operating Earnings were $28.2m and $55.9m, respectively.

NAT continues to maintain a strong balance sheet with low net debt and is focusing on keeping a low financial risk. At the end of 1Q2017, the Company had net debt of about $307m or about $10.2m per vessel based on a 30 vessels fleet.

World Economy and the Tanker Market

The development of the world economy affects the tanker industry and the demand for oil. The current demand for oil is increasing and the growth is particularly strong in China and India. NAT is very active in the Far East and does business with the major oil companies in the area.

The Suezmax fleet of the world (excl. shuttle tankers) counts 466 vessels at the end of 1Q2017, following an increase of eight vessels in the 1st quarter of 2017.

During the years 2014 and 2015, a number of orders were placed with shipyards. In 2016 twelve new ships were ordered at the shipyards including three from NAT. This is the lowest number of new orders since the mid-1990s. The current orderbook of Suezmax tankers stands at 65 vessels from now to the end of 2018. This represents about 14% of the Suezmax fleet. Slippage and cancellations may take place, thereby reducing the orderbook. In 2016, it was a fleet growth of 6.0% with no scrapping of vessels.

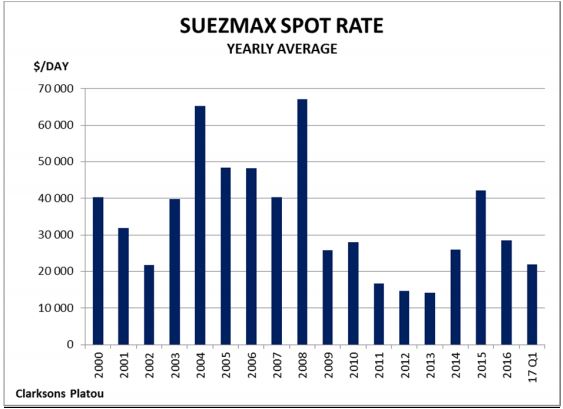

The graph to the below shows the average yearly spot rates since 2000 as reported by Clarksons Platou. The rates are an indication of the level of the market and its direction.

The supply of tanker tonnage is inelastic in the short term. When there are too many ships, rates tend to go down. When there is scarcity of ships, rates tend to go up.

Corporate Governance/Conflict of Interests

It is vital for NAT to ensure that there is no conflict of interests among shareholders, management, affiliates and related parties. Interests must be aligned. From time to time in the shipping industry, we see that questionable transactions take place which are not in harmony with sound corporate governance principles, both as to transparency and related party aspects. We have zero tolerance for corruption.

Strategy going forward

Our objective is to have a strategy that is flexible and has benefits in both a strong tanker market and a weak one. In an improved market, higher earnings and dividends can be expected. The Company is in a position to reap the benefits of strong markets.

Our dividend policy will continue to enable us to achieve a competitive cash yield.

NAT is firmly committed to protecting its underlying earnings and dividend potential. We shall endeavor to safeguard and further strengthen this position in a deliberate, predictable and transparent way.

Going forward we believe the recent acquisitions of vessels will increase the Total Return for NAT shareholders over time.

Full Report

Source: Nordic American Tankers Limited

HEADLINES

- Reversal! HMM Union Drops Opposition, Headquarters Relocation to Busan Confirmed

- Five Major Shipping Lines Have Over 30 Vessels Trapped in the Strait of Hormuz

- COSCO SHIPPING Holdings Achieves RMB 5.877 Billion in Net Profit Attributable to Parent Company in Q1 2026

- VLCC Idle Rate Climbs to 55%! Tanker Owners Grapple with Scarcity of Physical Cargoes

- COSCO SHIPPING Energy: Acquires 100% Equity of Dalian Investment; Q1 Net Profit Soars by 206.7%

- China's largest domestically built LNG carrier delivered