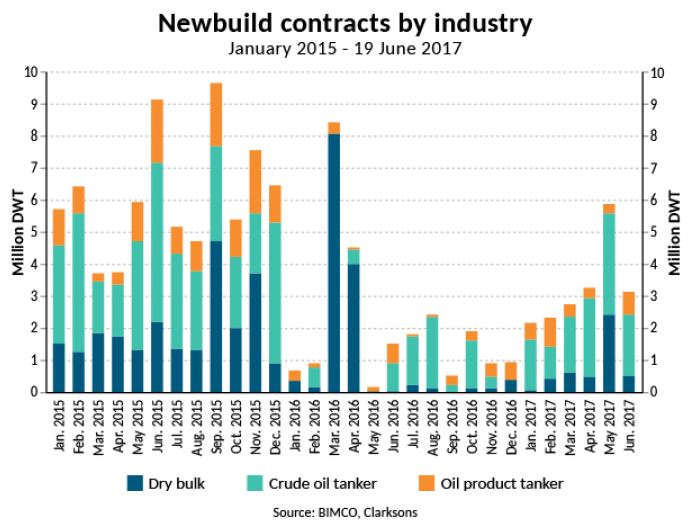

Dry bulk and tanker newbuild contracts 20% higher than 2016

Newbuild contracts have been signed for the dry bulk and tanker shipping industries at an increasing pace so far in 2017. The newbuild activity for the first half of 2017 has surpassed the same period last year by 20%. 5.9 million DWT was contracted in May 2017 and 3.1 million DWT so far in June 2017, which brings the total amount of newbuild orders up to 19.6 million DWT for 2017.

So far for June 2017, 22 tankers have been contracted amounting to a total of 2.6 million DWT. For the crude oil tanker segment, this has been entirely for suezmax ships with 1.9 million DWT ordered. The product tanker fleet has seen 0.7 million DWT ordered and 0.5 million DWT dry bulk ships contracted.

BIMCO’s Chief Shipping Analyst Peter Sand comments:” BIMCO expected newbuild activity to pick up, so the recent development is not surprising. It is however not what the industries needs given the present challenges in the market, as the earnings in all three segments gives little incentive for adding more capacity to the industry.

The low level of contracting as seen in 2016 – disregarding the 30 valemax ships ordered in March and April – is necessary in order to restore the fundamental balance between supply and demand in the shipping industry.

As the dry bulk -, crude oil – and oil product tanker shipping sectors are all struggling with very low freight rates, it is important that the recent development in contracting activity reflects a short-term trend. A continuous high level of newbuild activity will halt the current slow progressing improvement in the shipping markets”.

Highest newbuild contracting activity for VLCC’s since 2008

The crude oil tanker industry has been the main driver for the increase in newbuild activity covering the dry bulk and tanker shipping industry, as more than 60% of the contracts agreed was for crude oil tankers. For the first half of 2017 a total of 11.8 million DWT tankers was ordered, with VLCC grabbing the lion’s share of it. 71% of the newbuild orders for the crude oil tankers was VLCC’s being contracted, this amounts to a total of 8.5 million DWT and 27 ships. As all 27 VLCC ships were ordered between January and May 2017, it was the highest level of VLCC orders for the first five months since 2008. Furthermore, 2.2 million DWT suezmax ships and 1.1 million DWT of aframax ships have been ordered.

Highest VLCC net fleet growth for more than 7 years

The net fleet growth for the VLCC fleet reached 8.1% in February 2017, which is the highest level since September 2009. This was primarily due to the delivery of VLCC ships for the first five months of 2017 being the highest amount since 2011 and only two VLCC’s exiting trading so far in 2017.

The surge in deliveries has been injected directly into the supply side, as the demolition activity for the crude oil tanker shipping industry has been close to zero in a large part of 2015 and 2016. Thereby, the demolition activity hasn’t taken any supply out of the market and caused the fleet growth to climb similar to the deliveries. Chief Shipping Analyst Peter Sand adds:” BIMCO continuously stresses the need for managing the supply in the crude oil tanker industry. It is essential to handle the supply side as demand growth will not support the market to the same extent, as it did in 2016. If the situation doesn’t ease off, we might see the same fundamental imbalance for tankers, as seen in the dry bulk shipping industry, which will take years to overcome”.

Lowest dry bulk orderbook since 2004

Shipowners and investors in the dry bulk shipping industry have contracted 4.5 million DWT of newbuilds during the first five months of 2017. No capesize ships were contracted in the first four months of 2017, while a total of six capesize ships were contracted in May 2017 alone, with four of those being ore carriers larger than 300,000 DWT. Thereby, the six capesize orders added 1.6 million DWT to the orderbook for the dry bulk shipping industry. 2 million DWT of panamax ships were added to the orderbook during the first five months. 0.7 million DWT has been contracted for the handymax segment and 0.2 million DWT for the handysize segment.

The orderbook for the dry bulk shipping industry has declined from 185 million DWT in July 2014 to 61.3 million DWT in June 2017. This is the lowest orderbook level since April 2004 and indicates that a higher level of deliveries is being made every month, than newbuild contracts agreed. BIMCO will extend the series of analysis on the “Road to Recovery” for the shipping markets by looking at the crude oil tanker sector in the summer 2017.

Source: Peter Sand, Chief Shipping Analyst; BIMCO

HEADLINES

- Reversal! HMM Union Drops Opposition, Headquarters Relocation to Busan Confirmed

- Five Major Shipping Lines Have Over 30 Vessels Trapped in the Strait of Hormuz

- COSCO SHIPPING Holdings Achieves RMB 5.877 Billion in Net Profit Attributable to Parent Company in Q1 2026

- VLCC Idle Rate Climbs to 55%! Tanker Owners Grapple with Scarcity of Physical Cargoes

- COSCO SHIPPING Energy: Acquires 100% Equity of Dalian Investment; Q1 Net Profit Soars by 206.7%

- China's largest domestically built LNG carrier delivered