7.28-8.1 Global Dry Bulk Market Weekly Comment

A close examination of recent spot chartering activity shows that 97 dry bulk vessels were chartered in the spot market last week. This is 23 less than were chartered during the previous week. Last week's vessel chartering activity included the chartering of 31 capesize vessels (9 less than the previous week), 42 panamax vessels (6 less than the previous week), 14 handymax vessels (8 less than the previous week), and 10 handysize vessels (the same amount as the previous week). Despite the large decline in chartering activity, overall dry bulk freight rates found a level of support last week. Capesize rates ended last week averaging $8,522 /day, a decline of $99 (1%) from a week ago. Panamax rates ended last week averaging $4,859/day, an increase of $23 from a week ago. Supramax rates ended last week averaging $7,608/day, an increase of $511 (7%) from a week ago. Handysize rates ended last week averaging $5,357/day, a decrease of $26 from a week ago.

Looking at dry bulk cargo trends in specific detail, a particularly large amount of Australian iron ore cargoes and South American grain cargoes surfaced in the market again last week. In total, 20 Australian iron ore cargoes surfaced in the market last week. This was 8 less than surfaced during the previous week but still a very firm amount. The Australian iron ore cargoes will be shipped to various buyers in Asia, mostly to buyers in China. In addition, 12 South American grain cargoes came to the market last week. This is 5 less than surfaced during the previous week but also a firm amount. The South American grain cargoes will be shipped to various buyers around the world.

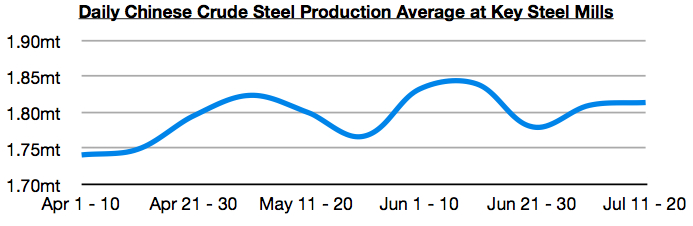

In China, recently data from the China Iron and Steel Association (CISA) shows that steel production has remained at a near record level. Average daily crude steel production at China's key steel mills totaled approximately 1.81 million tons during July 11 to July 20. This is the same level seen during the previous ten days, and is very close to the record 1.84 million ton average seen during June 21 to June 30. Several new construction projects continue to be approved in China and the government also continues to work towards further stimulating the economy. In addition, this year’s substantial decline in global iron ore prices has allowed profit margins at Chinese steel mills to remain much improved from the start of this year. Chinese steel production (and demand for imported iron ore cargoes in the dry bulk shipping market) is set to remain very strong.

Chart is attached (data is in million tons).

HEADLINES

- Reversal! HMM Union Drops Opposition, Headquarters Relocation to Busan Confirmed

- Five Major Shipping Lines Have Over 30 Vessels Trapped in the Strait of Hormuz

- COSCO SHIPPING Holdings Achieves RMB 5.877 Billion in Net Profit Attributable to Parent Company in Q1 2026

- VLCC Idle Rate Climbs to 55%! Tanker Owners Grapple with Scarcity of Physical Cargoes

- COSCO SHIPPING Energy: Acquires 100% Equity of Dalian Investment; Q1 Net Profit Soars by 206.7%

- China's largest domestically built LNG carrier delivered