The Cold Winds Doth Blow, Still…

The shipping markets have in the main been pretty icy since the onset of the global economic downturn back in 2008, but 2016 has seen a particular blast of cold air rattle through the shipping industry, with few sectors escaping the frosty grasp of the downturn. Asset investment equally appears to have been frozen close to stasis. So, can we measure how cold things have really been?

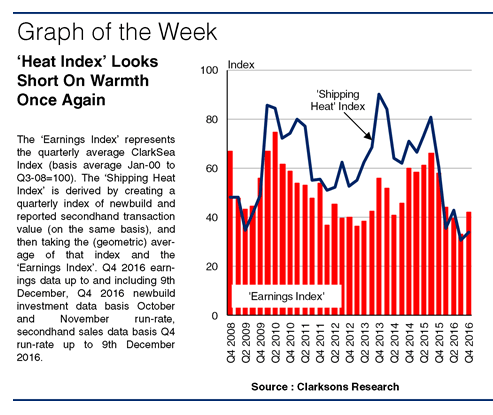

Lack Of Heat

Generally, our ClarkSea Index provides a helpful way to take the temperature of industry earnings, measuring the performance of the key ‘volume’ market sectors (tankers, bulkers, boxships and gas carriers). Since the start of Q4 2008 it has averaged $11,948/day, compared to $23,666/day between the start of 2000 and the end of Q3 2008. However, earnings aren’t the only thing that can provide ‘heat’ in shipping. Investor appetite for vessel acquisition has often added ‘heat’ to the market in the form of investment in newbuild or secondhand tonnage, even when, as in 2013, earnings remained challenged. To examine this, we once again revisit the quarterly ‘Shipping Heat Index’, which reflects not only vessel earnings but also investment activity, to see how iced up 2016 has really been.

Fresh Heat?

This year, we’ve tweaked the index a little, to include historical newbuild and secondhand asset investment in terms of value, rather than just the pure number of units. This helps us better put the level of ‘Shipping Heat’ in context. In these terms, shipping appears to be as cold (if not more so) as back in early 2009. This year the ‘Heat Index’ has averaged 36, standing at 34 in Q4 2016, which compares to a four-quarter average of 43 between Q4 2008 and Q3 2009.

Feeling The Chill

Partly, of course, this reflects the earnings environment. The ClarkSea Index has averaged $9,329/day in the year to date and is on track for the lowest annual average in 30 years. In August 2016, the index hit $7,073/day, with the major shipping markets all under severe pressure.

All Iced Up

The investment side has seen the temperature drop even further. Newbuilding contracts have numbered just 419 in the first eleven months of 2016, heading for the lowest annual total in over 30 years, and newbuild investment value has totalled just $30.9bn. Weak volume sector markets, as well as a frozen stiff offshore sector, have by far outweighed positivity in some of the niche sectors (50% of the value of newbuild investment this year has been in cruise ships). S&P volumes have been fairly steady, but the reported aggregate value is down at $11.2bn. All this has led to the ‘Shipping Heat Index’ dropping down below its 2009 low-point.

Baby It’s Cold Outside

So, in today’s challenging markets the heat is once again absent from shipping. And, in fact, on taking the temperature, things are just as icy as they were back in 2008-09 when the cold winds of recession blew in. This year has shown that after years out in the cold, it’s pretty hard for things not to get frozen up. Let’s hope for some warmer conditions in 2017.

Source: Clarksons

HEADLINES

- Reversal! HMM Union Drops Opposition, Headquarters Relocation to Busan Confirmed

- Five Major Shipping Lines Have Over 30 Vessels Trapped in the Strait of Hormuz

- COSCO SHIPPING Holdings Achieves RMB 5.877 Billion in Net Profit Attributable to Parent Company in Q1 2026

- VLCC Idle Rate Climbs to 55%! Tanker Owners Grapple with Scarcity of Physical Cargoes

- COSCO SHIPPING Energy: Acquires 100% Equity of Dalian Investment; Q1 Net Profit Soars by 206.7%

- China's largest domestically built LNG carrier delivered